Gold prices in Pakistan fell on Tuesday, mirroring a decrease in international rates. In the local market, the price of gold per tola dropped by Rs1,000, bringing it down to Rs261,500, according to figures from the All-Pakistan Gems and Jewellers Sarafa Association (APGJSA).

The price of 10-gramme gold also decreased, shedding Rs857 to settle at Rs224,194. This decline follows a period of stability, as gold prices remained unchanged at Rs262,500 per tola on Monday.

Last month, gold prices in Pakistan reached an all-time high of Rs263,700 per tola, causing concern among non-investors, potential buyers, and individuals purchasing the precious metal for weddings or as a safeguard for their earnings.

On the international front, gold prices also saw a reduction on Tuesday. APGJSA reported that the international rate stood at $2,498 per ounce (including a $20 premium), marking a decrease of $5 for the day.

Meanwhile, silver prices remained stable at Rs2,950 per tola.

Federal Minister for Finance and Revenue, Senator Muhammad Aurangzeb, announced on Tuesday that the government is nearing the finalisation of external financing assurances, a crucial step toward securing the $7 billion loan from the International Monetary Fund (IMF).

Speaking at a briefing, Aurangzeb expressed confidence that the IMF’s Executive Board would approve the programme soon, acknowledging the support from provincial governments.

Aurangzeb reiterated Prime Minister Shehbaz Sharif’s assertion that this would be Pakistan’s last programme with the IMF, underlining the necessity of implementing structural reforms to ensure long-term economic stability.

In July, Pakistan and the IMF reached a staff-level agreement on a 37-month Extended Fund Facility (EFF) worth around $7 billion. However, the programme’s approval by the IMF’s Executive Board is contingent on Pakistan securing financing assurances from its development partners, a process that is still ongoing.

Pakistan is actively working to secure a rollover of $12 billion in loans from key allies, including China, Saudi Arabia, and the UAE. Additionally, the country has requested an extra $1.2 billion loan from Saudi Arabia to address a $2 billion financing gap.

Aurangzeb highlighted improvements in economic indicators, noting that the government has cleared all pending payments, including import letters of credit and profit remittances.

He pointed out that inflation has decreased to 9.6 per cent in August 2024 from 23.7 per cent in the same period last year, leading to a gradual reduction in the policy rate, which is providing relief to the industrial sector.

The Minister also cited improvements in Pakistan’s credit ratings by agencies like Fitch and Moody’s as evidence of the economy’s positive trajectory.

On tax collection, Aurangzeb emphasised the government’s determination to increase revenue, noting that a significant portion of the economy contributes minimally to the tax base. He stressed the need for broader tax compliance and assured that the Federal Board of Revenue (FBR) has simplified the tax filing process.

Despite a shortfall of Rs 98 billion in tax collection during the first two months of the fiscal year, he reaffirmed the government’s commitment to not delay necessary processes.

Aurangzeb also addressed rightsizing the federal government and introduced plans for a new subsidy mechanism aimed at enhancing transparency.

He reassured stakeholders that any decisions regarding the Utility Stores Corporation (USC) would be made with employee and stakeholder interests in mind, emphasising the government’s commitment to protecting jobs and well-being.

The International Monetary Fund (IMF) has put forward at least three strict conditions in Pakistan after the Punjab province gave Rs45 to Rs90 billion in electricity subsidies for two months.

Last month, President of Pakistan Muslim League-Nawaz Muhammad Nawaz Sharif announced that Punjab government would provide relief of fourteen rupees per unit to consumers using up to 500 units of electricity in August and September bills.

The IMF has asked the province to end the temporary subsidy by September 30th while also clarifying that no province w could give such a subsidy during the 37-month Extended Fund Facility (EEF) programme.

According to IMF, it was one of the conditions for the bailout that no provinces would take such a move. This brings into question Prime Minister Shehbaz Sharif’s previous statement when he encouraged other provinces to follow suit of Punjab.

Tribune reported that the IMF also introduced the condition that would bind the provinces to not introduce any fiscal policy that could undermine the commitments given under $7 billion loan.

The provinces have committed to signing a National Fiscal Pact by the end of September, which would mean they undertake some expenditures that are currently the federal government’s responsibility.

Pakistan’s inflation rate dropped to 9.6 per cent in August 2024, a significant decrease from the 11.1 per cent recorded in July 2024, according to data from the Pakistan Bureau of Statistics (PBS).

This marks the first time in three years that inflation has returned to single digits, with the last instance being in October 2021 when it stood at 9.2 per cent.

On a month-to-month basis, the Consumer Price Index (CPI) saw a modest rise of 0.4 per cent in August 2024, compared to a 2.1 per cent increase in July 2024 and a 1.7 per cent rise in August 2023.

This slowdown in monthly inflation aligns with the predictions of the Ministry of Finance, which had anticipated inflation to fall between 9.5 per cent and 10.5 per cent in its recent economic outlook.

The Finance Ministry also suggested that if the current economic stability continues, inflation could drop further to between 9 per cent and 10 per cent by September 2024.

This decline in inflation follows the State Bank of Pakistan’s (SBP) decision to reduce the key policy rate by 100 basis points to 19.5 per cent in July.

The SBP had warned of potential inflation risks due to fiscal issues and sudden changes in energy prices, but the recent figures show a positive trend.

Inflation has been a major issue for Pakistan, especially after hitting a record high of 38 per cent in May 2023. However, it has been steadily decreasing since then.

The recent inflation data also matched projections from various financial institutions. JS Global, a brokerage firm, had predicted a 9.3 per cent inflation rate, noting that this would be the first time in three years that inflation dropped into single digits.

They believe this trend could lead to further interest rate cuts, with the policy rate possibly dropping to 18 per cent in September 2024.

Prime Minister Shehbaz Sharif on Sunday expressed his satisfaction with the recent ease in the inflation rate, noting that the government’s ongoing economic reforms are yielding positive results.

In a recent statement, PM Shehbaz highlighted that the recent upgrade in Pakistan’s credit rating by Moody’s was a clear acknowledgment of the country’s improving economic indicators. He said that international institutions are recognising the progress Pakistan is making.

Moody’s Ratings recently upgraded Pakistan’s local and foreign currency issuer and senior unsecured debt ratings from Caa3 to Caa2. This upgrade reflects slightly better macroeconomic conditions, alongside improved government liquidity and external positions, which, although still weak, have shown improvement. According to Moody’s, Pakistan’s default risk has now decreased.

This development follows another upgrade in July when Fitch Ratings pushed Pakistan’s Long-Term Foreign-Currency Issuer Default Rating (IDR) from ‘CCC’ to ‘CCC+’.

The Prime Minister expressed satisfaction with the Consumer Price Index (CPI) easing to 11 per cent in July, and he anticipates that it will decline further in August. He reiterated the government’s commitment to pursuing economic reforms, including a right-sizing policy, which he is personally overseeing to ensure rapid implementation.

PM Shehbaz expressed confidence that the reforms would soon have a noticeable positive impact on the country’s economy. He reassured the public that the government is fully aware of the challenges faced by the people and is working to address them.

The government has marginally reduced petrol prices by Rs1.86 per litre for the next two weeks, following approval from Prime Minister Shehbaz Sharif.

This slight decrease falls short of the anticipated Rs6 per litre, with many Pakistanis expecting a reduction of at least Rs3.10 per litre.

Effective from September, the new petrol price in Pakistan will be Rs259.10 per litre, down from Rs260.96. The price of high-speed diesel (HSD) has also been lowered by Rs3.32 per litre, bringing it down to Rs262.75 from Rs266.07.

Additionally, the prices of kerosene oil and light diesel oil have been cut by Rs2.15 and Rs2.97 per litre, respectively, reducing their prices to Rs169.62 and Rs154.05 per litre.

This marks the third consecutive reduction in petroleum product prices, with a total decrease of Rs16.5 per litre for petrol since July 30. In the previous fortnightly review, petrol and diesel prices were reduced by Rs8.47 and Rs6.70 per litre, respectively.

It remains unclear whether this minimal price reduction will impact public transport fares or ride-hailing services, and it is unlikely to significantly ease daily commuting costs for motorists. Nonetheless, the prices are decreasing rather than rising.

Pakistan’s headline inflation is expected to ease further in August 2024, settling between 9.5 per cent and 10.5 per cent, with a continued downward trend anticipated in the coming months, according to the Finance Division’s statement on Friday.

The Ministry of Finance, in its ‘Monthly Economic Update and Outlook’, highlighted that the inflation rate could drop even further to between 9 per cent and 10 per cent by September 2024, attributed to the stabilisation of key economic indicators.

July 2024 saw headline inflation at 11.1 per cent year-on-year, a decrease from 12.6 per cent in June 2024. This marks the lowest Consumer Price Index (CPI) figure since November 2021, when inflation was recorded at 11.5 per cent, as per data from the Pakistan Bureau of Statistics (PBS).

The Finance Ministry’s report also pointed to positive trends in external indicators such as exports, imports, and workers’ remittances, which are on an upward trajectory.

A brokerage house noted that August’s inflation figure is expected to dip into single digits for the first time in nearly three years.

Looking ahead, the report projects that exports will range between $2.5 billion and $3.2 billion, imports between $4.5 billion and $5 billion, and remittances between $2.6 billion and $3.3 billion in August 2024.

The stable outlook for the external sector is contingent upon factors including a stable exchange rate, revived domestic economic activities, improved agricultural output, lower domestic and global commodity prices, and increased foreign demand.

In the industrial sector, the Ministry of Finance anticipates that the Large Scale Manufacturing (LSM) sector will maintain its positive growth trajectory in FY2025, driven by improved external demand, a stable exchange rate, declining inflation, and a more accommodating monetary policy.

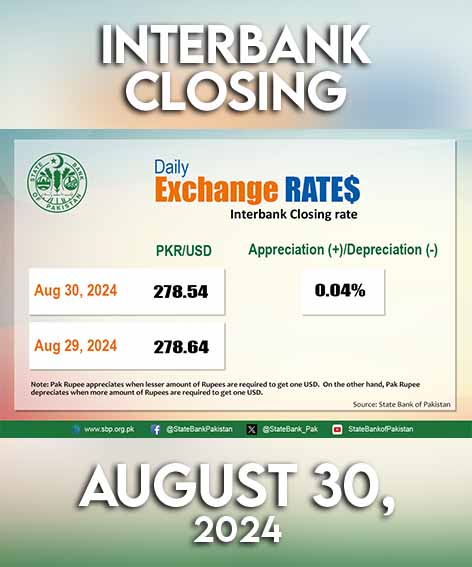

The Pakistani rupee (PKR) continued its trend of minimal fluctuations, appreciating by 10.44 paisa or 0.04 per cent against the US dollar (USD) during Friday’s interbank session.

The PKR closed at 278.54 per USD, up from the previous close of 278.64 on Thursday.

In the open market, exchange companies quoted the dollar at 279.15 for buying and 280 for selling. Throughout the day, the currency reached an intraday high (bid) of 279 and a low (ask) of 278.90.

Over the week, the PKR recorded a total loss of 4 paisa against the greenback.

Here’s how Pakistani currency performed on last trading day of the week against other currecnies:

Currency

Friday’s value

Change

Thursday’s value

Saudi Riyal

74.23

-2.78 paisa

74.26

UAE Dirham

75.86

+2.85 paisa

75.84

Euro

308.8

-79.84 paisa

309.6

Swiss Franc

328.41

-2.35 rupees

330.75

British Pound

367.35

-72.28 paisa

368.07

Japanese Yen

1.921

-0.5 paisa

1.926

Chinese Yuan

39.29

+9.14 paisa

39.2

Exchange rates for Friday

Against major currencies, the Saudi Riyal closed at 74.23, losing 2.78 paisa from the previous day’s value of 74.26. The UAE Dirham decreased by 2.85 paisa, closing at 75.86, down from 75.84.

Meanwhile, the PKR gained 79.84 paisa against the Euro, closing at 308.8 compared to the previous value of 309.6. The Swiss Franc dropped by 2.35 rupees, ending the session at 328.41, down from 330.75.

The British Pound became cheaper by 72.28 paisa, closing at 367.35 compared to 368.07 the day before. Against the Japanese Yen, the PKR gained 0.5 paisa, closing at 1.921 versus 1.926 the previous day. The Chinese Yuan saw an increase of 9.14 paisa, closing at 39.29 compared to 39.2 in the previous session.

In recent months, the domestic currency has remained in the range of 277-279, with traders closely monitoring the approval of a new $7-billion Extended Fund Facility by the International Monetary Fund’s (IMF) Executive Board.

During the current financial year, the PKR has depreciated against the dollar by 19.67 paisa or 0.07 per cent. However, the currency has appreciated by 3.32 rupees or 1.19 per cent in the current calendar year.

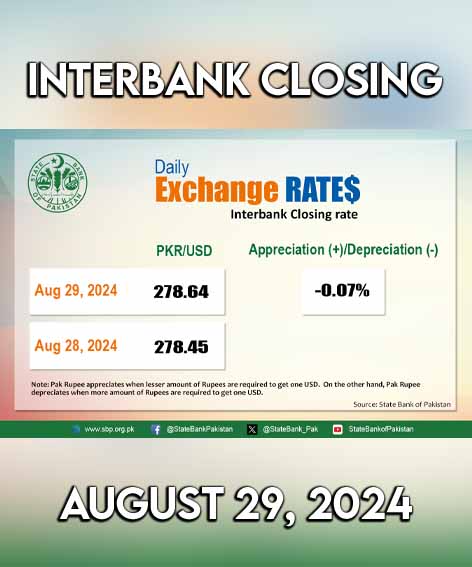

On Thursday, the Pakistani rupee (PKR) saw a slight depreciation of 19.23 paisa, or 0.07 per cent, against the US dollar (USD) in the interbank market.

The rupee settled at PKR 278.64 per USD, compared to the previous closing rate of PKR 278.45. Throughout the trading session, the rupee reached an intraday high bid of PKR 278.80 and an intraday low ask of PKR 278.70.

In the open market, exchange companies quoted the USD at PKR 279.13 for buying and PKR 280 for selling.

Here’s how Pakistani currency performed against other major currencies:

Currency

Change

Previous rate

Thursday’s rate

Swiss Franc

+50.26 paisa

330.25

330.75

British Pound

-38.65 paisa

368.46

368.07

Euro

+1.12 rupee

310.72

309.60

Chinese Yuan

+13.78 paisa

39.06

39.20

Japanese Yen

+0.01 paisa

1.9261

1.926

Saudi Riyal

+4.93 paisa

74.21

74.26

UAE Dirham

+5.24 paisa

75.86

75.81

PKR exchange rates for Thursday

In comparison to other major currencies, the Swiss franc gained 50.26 paisa, closing at PKR 330.75, up from PKR 330.25 in the previous session. Conversely, the British pound depreciated by 38.65 paisa, settling at PKR 368.07, compared to PKR 368.46 from the day before.

The PKR also strengthened against the Euro, gaining 1.12 rupees to close at PKR 309.60, up from PKR 310.72. The Chinese yuan saw an increase of 13.78 paisa, closing at PKR 39.20 compared to PKR 39.06 previously.

Against the Japanese yen, the PKR gained 0.01 paisa, ending at PKR 1.926, compared to PKR 1.9261 a day earlier. The Saudi riyal closed at PKR 74.26, reflecting a gain of 4.93 paisa from PKR 74.21 the previous day. The UAE dirham appreciated by 5.24 paisa, closing at PKR 75.81 compared to PKR 75.86.

In recent months, the PKR has largely fluctuated between PKR 277 and PKR 279 as traders await approval from the International Monetary Fund’s (IMF) Executive Board for a new $7 billion Extended Fund Facility. In a positive development,

Moody’s Ratings upgraded Pakistan’s local and foreign currency issuer and senior unsecured debt ratings from Caa3 to Caa2. Moody’s also anticipates IMF approval for Pakistan’s Extended Fund Facility in the coming weeks.

Globally, the US dollar stabilised on Thursday, recovering some of its previous losses. Traders are now looking forward to a key US inflation report at the end of the week, which may provide further insights into the future direction of interest rates.

So far in the current financial year, the PKR has depreciated against the dollar by 30.11 paisa, or 0.11 per cent. However, for the calendar year, the PKR has appreciated by 3.22 rupees, or 1.16 per cent.

Foreign exchange reserves held by the State Bank of Pakistan (SBP) saw a rise of $112 million over the past week, bringing the total to $9.4 billion as of August 23, according to data released on Thursday.

“During the week ending on August 23, 2024, SBP reserves increased by $112 million, reaching $9.4 billion,” the bank stated in its report. This follows a smaller increase of $19 million the previous week.

In total, the country’s liquid foreign reserves reached $14.77 billion, with commercial banks holding $5.37 billion of this amount. The central bank did not provide any specific reason for the increase in its reserves.

The rise in reserves comes as Pakistan seeks to raise up to $4 billion from Middle Eastern commercial banks by the next fiscal year (FY26). This effort is part of a broader strategy to address the country’s external financing needs, as explained by SBP Governor Jameel Ahmad in a recent interview.

Ahmad also mentioned that Pakistan is in the final stages of securing an additional $2 billion in external funding, which is crucial for obtaining the International Monetary Fund (IMF) approval for a $7 billion bailout programme.

In related financial news, the international price of gold rose to $2,516 per ounce on Thursday, marking an increase of $4 during the day, according to the All Pakistan Gems and Jewellery Traders and Exporters Association (APGJSA). Silver prices, however, remained steady at Rs2,950 per tola.